Simplifying HMO vs PPO.

Most people we meet with have heard of HMOs and PPOs, but aren’t sure how they’re different. Each is a type of managed care that uses a network of doctors, hospitals, and healthcare facilities to offer a cost-effective alternative to traditional plans. Let’s take a look at each:

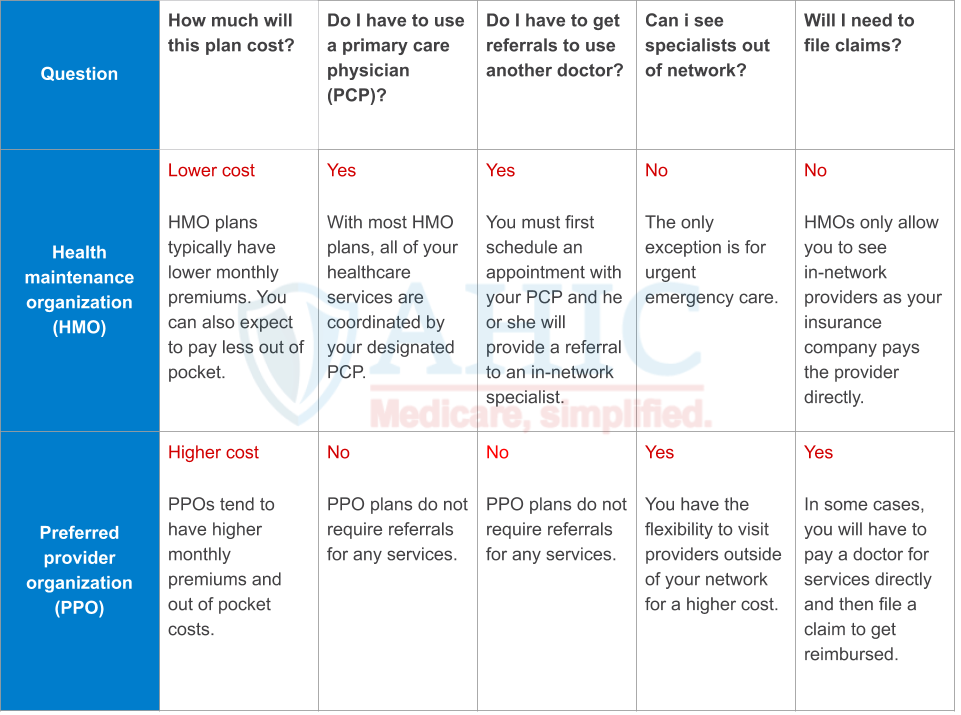

HMO

A Health Maintenance Organization (HMO) uses their own network of doctors, hospitals and other healthcare providers who have all agreed to provide a service for an agreed upon payment. A HMO requires you to stay within its network to receive health services, and may referrals and prior authorization. Generally, you’ll choose or be assigned a Primary Care Physician (PCP) that will help you coordinate additional care.

For example: If you’re suffering from shoulder pain, you’d first need to be examined by your PCP who will determine if you need to see a specialist. If you do, your PCP will refer you to a specialist in your network for additional care.

You’ll need to stay in your network, with some exceptions:

- Emergency and urgently needed services received outside of the network are covered.

- When the enrollee is temporarily absent from the plan’s service area, dialysis services are covered.

- If the network does not have a necessary specialist that you require.

Is an HMO right for you?

HMOs are generally very cost effective. They have lower monthly premiums, copays, and often bundle extras beyond what Medicare covers. But, there are some major things to consider:

What networks are available to you?

The networks available depend on where you live. Not all networks are created equal, so your selection, based on your situation, is important. If you want to visit specific doctors, hospitals, and facilities, you’ll need to choose the plan that gives you access. An agent can help you find out which networks are available and include the facilities and doctors you want.

Is using a Primary Care Provider right for you?

Are you okay with having your PCP be the gatekeeper to your healthcare? Often, getting a referral is quick and easy, and may even help you develop a better relationship with your doctor. Having one person guide your decision making can be a good thing. However, some people don’t like spending the extra time required to get a referral or don’t want to be limited in the physicians they can see. People in this camp don’t mind the extra responsibility of managing their own care because they have more freedom.

How do the costs compare?

HMOs are generally less costly than PPOs, at the expense of staying in-network. If cost is a major factor then HMO should be a consideration.

PPO

Preferred Provider Organization (PPO), like HMO, offers a network of healthcare providers for your medical care. The major difference is you have the option to use the network, or for a higher cost, you can go outside of the network.

A PPO offers you the freedom and flexibility to receive care from any provider. This means you can visit any doctor, specialist, or hospital without a referral. This also means you do not have to have an assigned PCP.

Is a PPO right for you?

This decision is a little more straightforward. If you want the option to visit any care provider without a referral, and are willing to pay more, a PPO may be for you.

How do the costs compare?

Choice is what makes PPOs great, but it also makes them more expensive.Your monthly premiums will be higher and your copays for office visits will cost more. Additionally, you’ll have an annual deductible you’ll need to meet before the plan pays for some or all services. To help reduce costs, you can use the “Preferred Providers” in-network. This list of providers will have a lower copay compared to out-of-network providers.

We’re on your side

If you’re still not sure which to choose, you’re not alone. AHIC is here to walk you through the process of applying for Medicare or shopping for the plan that’s right for you. Our services are free for you and we’ll be here to help for the lifetime of your policy.